Australia’s online consumers are onboard the Buy Now, Pay Later train and it’s full steam ahead. This financial flexibility in purchasing has pivoted the digital landscape permanently. The forced shift to digital due to the pandemic has further cemented consumer reliance on online payment options and a cashless society.

With multiple new BNPL solutions infiltrating the market it can be difficult as a retailer to know what is best received by your customers online.

We have consolidated the key statistics on who uses what to help you customise your online payment process for your target market.

What is BNPL?

Firstly we’ll cover the basics of what Buy Now, Pay Later is.

Remember layby? Customers would request for a product to be put aside and the cost would be paid off in installments before receiving the goods.

BNPL adopts a similar principle of payment installments, however the BNPL institution takes on this financial burden upfront so the customer receives their goods immediately. The repayments are deducted from the customer’s account on a regular basis with late fees applied for failure to pay on time.

What does BNPL mean for retailers? (in a brief summary)

- Boost to your bottom line

- Increase average order value and frequency

- Reduce the financial barriers to entry for your customers

- Create simplicity in the customer journey through a frictionless one-click purchasing process

- Locked in contract with the BNPL provider (typically 12 months)

- Fixed cost charge per transaction via the BNPL provider (approximately 4% on every transaction)

Who uses it?

By Gender

According to Roy Morgan, women are twice as likely to use BNPL services with 11.6% of females reporting use compared to 5.5% of men.

By Age

To not surprise, customers under 35 years dominate the BNPL market – accounting for 55.9% of users while they represent only 18% of the Australian population. Young users tend to be early adopters of such innovative solutions and have the financial limitations to warrant these services.

In comparison, our baby boomers account for 40.7% of the population but only 14.2% of pay-later users.

By Wealth

Employed, low income earners tend to use pay-later solutions. Australians earning between $40,000 to $49,999 per annum represent 11.7% of pay-later users compared to those earning <$150,000 per annum representing only 2.2% of users.

What does indicate for retailers?

For retailers that target the young, female market, it indicates that a wider variety of pay-later services should be available at checkout to more effectively meet consumer expectations and purchasing habits.

Reliance on pay-later solutions aren’t as necessary for premium, high-end retailers who target higher income earners. Though consumer flexibility in purchasing options should also be considered.

What pay-later solution should you be using as a retailer?

One in ten Australians use BNPL services in an average twelve-month period according to Roy Morgan research from November 2019 (up from 6.8% in 2018). It can be expected that this trajectory will continue in coming years due to more permanent shift to contact-free purchasing.

Of this, Afterpay dominates the market at 9%, followed by Zip Pay at 2.4% and Zip Money used by 1.2%.

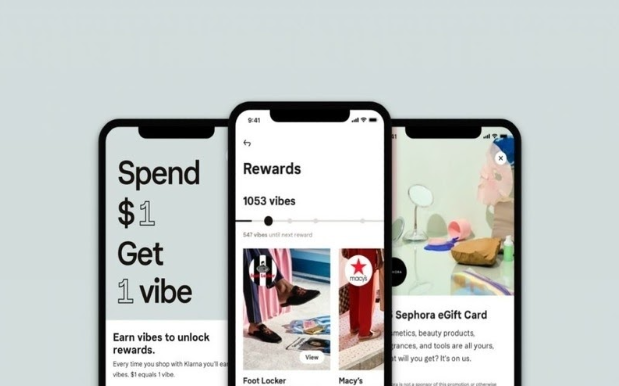

Since this study was conducted, new players have emerged into the Australian market. Swedish based BNPL provider Klarna launched in January 2020 and partnered with Commonwealth Bank. They are the first BNPL to release ‘Vibe’ a points-based rewards program to be rolled out in Australia later in the year.

In summary

Would you have a store that only accepted Visa and not Mastercard?

A single buy-now-pay-later solution on in-store & online checkout doesn’t cut it these days, with the market share of BNPL providers spanning across several key players it’s crucial to offer your customers diversity.